The first phase of the AI economy rewarded those who created intelligence. The next phase may reward those who can turn intelligence into operational advantage.

Much of today’s AI narrative remains focused on foundation models, compute capacity, and algorithmic breakthroughs. Yet as AI capabilities become increasingly accessible and performance gaps gradually narrow, the basis of competition is beginning to shift. Competitive advantage is moving away from intelligence creation and toward the ability embed intelligence into real-world operations.

From autonomous factories and intelligent supply chains to software-defined vehicles and industrial robotics, AI is moving beyond digital workflows and into physical systems. The defining challenge is no longer whether AI can generate intelligence, but whether organizations can convert that intelligence into measurable improvements in productivity, quality, utilization, and economic performance. The next AI value pool may emerge not from creating more intelligence, but from embedding intelligence into the physical systems that drive economic output.

The Next AI Frontier Lies Beyond Knowledge Work

Generative AI has already reshaped writing, coding, search, customer support, and analytics. Those gains are real, but they are still concentrated in knowledge work. The larger economic prize sits elsewhere, in environments where AI can improve throughput, reduce downtime, optimize routing, raise yield, or replace repetitive physical tasks. That is the difference between productivity software and industrial execution. The first changes how people work; the second changes how enterprises operate. In other words, the opportunity is shifting from generating information to improving how physical systems operate and create economic value.

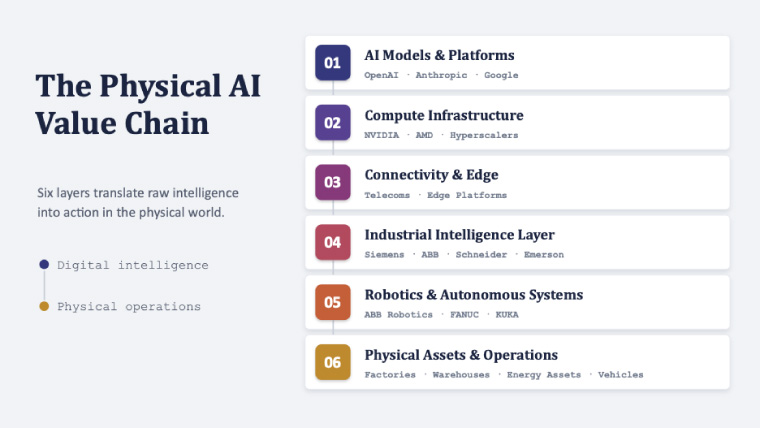

Convergence of AI and Physical Systems

Physical AI refers to the deployment of AI into physical systems such as factories, vehicles, machines, and infrastructure, enabling those systems to perceive, decide, and act autonomously. Physical AI is becoming practical now because several technology curves have matured together. Advances in AI models, robotics, and infrastructure have reached a point where large-scale deployment is increasingly feasible. The point is not that one breakthrough solved the problem. The point is that the stack finally came together. More importantly, this convergence is changing the economics of industrial implementation. Tasks that were previously too complex or too expensive to automate are increasingly becoming commercially viable.

That convergence is already visible in industrial strategy. Hyundai Motor Group was recently reported to be moving toward full ownership of Boston Dynamics, and Hyundai’s own CES 2026 materials show Atlas and Spot being positioned for industrial robotics and logistics use cases rather than as research toys. Robotics is being treated less as a future concept and more as a deployable operating capability.

Where the Next AI Value Pool Emerges

The most valuable physical AI use cases are likely to emerge where assets are expensive, processes are repetitive, and operating errors are costly. These environments share a common characteristic: even marginal improvements in productivity, utilization, quality, or throughput can generate significant economic returns. As a result, some industries are structurally better positioned than others to capture value from AI adoption.

Manufacturing

Manufacturing represents one of the largest potential value pools for physical AI. Large asset bases, labor-intensive operations, and highly measurable productivity economics create strong incentives to deploy AI across production systems. Even modest improvements in throughput, equipment, utilization, or product quality can create meaningful economic value when applied across large-scale manufacturing networks. As a result, manufacturers are increasingly deploying AI to optimize production flows, quality control, and asset performance.

Mobility

A similar dynamic is emerging in mobility. As vehicles evolve into increasingly software-defined and autonomous platforms, AI is becoming integral to vehicle operations, predictive maintenance, fleet management, and mobility services. The opportunity extends beyond the vehicle itself to the broader transportation ecosystem, where AI can improve asset utilization, operational efficiency, and service delivery at scale.

Logistics

Logistics may become one of the earliest large-scale deployment markets for physical AI because operations are already structured enough to automate while remaining complex enough to benefit from AI-driven optimization.

JD.com’s Richard Liu recently suggested that delivery operations could eventually be replaced by robots,. Whether or not the transition happens quickly, the strategic signal is clear: logistics is moving from labor-intensive execution toward machine-enabled execution.

Semiconductors

Semiconductor manufacturing is another compelling deployment environment for physical AI. Fab operations are data-rich, capital-intensive, and highly sensitive to small performance improvements. As a result, AI is being applied to yield optimization, defect detection, process control, and materials discovery.

The trend is already visible across the industry. Lam Research recently announced plans to embed sensing and AI capabilities into chipmaking equipment to improve productivity, highlighting that AI is not only consuming semiconductors but also becoming part of semiconductor production itself. In semiconductor manufacturing, even marginal improvements in throughput, utilization, or defect rates can translate into substantial financial value, making physical AI attractive.

From Models to Deployment

The model may answer questions, but business value is determined by whether intelligence improves revenue, cost, throughput, yield, or service quality. In this environment, the challenge is no longer generating intelligence but translating it into measurable operational outcomes.

This shift reflects a broader move from demonstration to production, from pilot to scale, and from software performance to operational impact. A company can buy access to a model; it cannot easily buy the operational discipline, proprietary data, domain expertise, and systems integration required to make that model work inside a factory, a fleet, or a supply chain.

Physical AI is not only about AI models and robots. It also depends on the broader industrial technology stack that connects intelligence to execution. Sensors, machine vision systems, industrial controllers, edge computing platforms, industrial software, and digital twins increasingly serve as the interface between AI-driven decision making and physical operations. As a result, the opportunity extends beyond robotics vendors to a much wider ecosystem of automation, industrial software, and operational technology providers.

The New Source of Competitive Advantage

In this context, the winner of the next AI economy may not be the companies that create intelligence but the companies that deploy it at scale. Value creation will increasingly depend on how effectively organizations embed AI into assets, workflows, and feedback loops that govern production, logistics, mobility, and infrastructure. The defining question is no longer what AI can do in isolation, but how much value it can create once embedded into real-world operations.