Overview of the Export Halt Situation in India

As India approaches its Rabi season, the recent specialty fertilizer export halt from China presents both challenges and significant opportunities for domestic Indian fertilizer producers. While China has been restricting supplies of specialty fertilizers to India for the last 4-5 years, a complete halt impacts a ~80% of specialty fertilizers supply for high-value crops such as fruits and vegetables, affecting agricultural belts in Maharashtra, Gujarat, Tamil Nadu, Uttar Pradesh and West Bengal.

An estimated 130-140 KT of specialty fertilizers were imported from China between June-December 2024, alone. Notable products include controlled-release fertilizers (CRFs) such as polymer-coated urea (PCU), chelated micronutrients (Fe-EDTA, Zn-EDTA, Fe-EDDHA), water-soluble fertilizers (WSFs) such as monoammonium phosphate (MAP) and potassium nitrate (KNO₃); and stabilized nitrogen fertilizers with urease inhibitors (NBPT). There are fears of price rises, as availability is not expected to be a major challenge. India has alternative import options from Russia, Jordon, and Israel; however, timely shipment arrival remains a concern.

Specialty Fertilizer Market Scenario & Growth Drivers

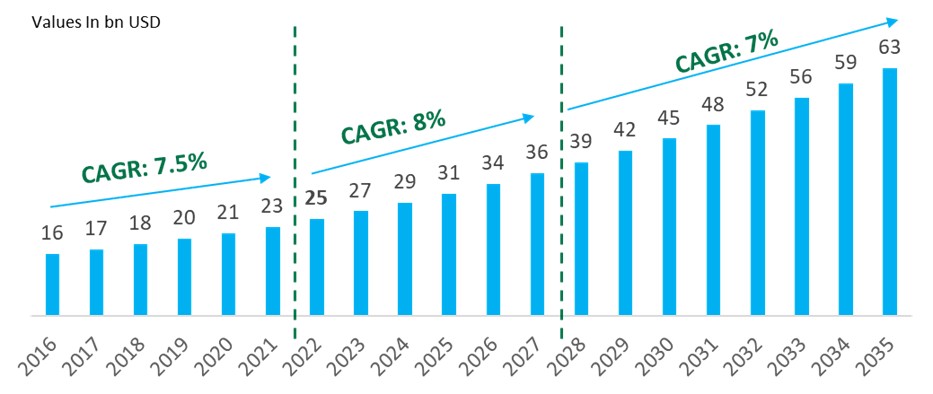

The Specialty Fertilizer Market has strong growth potential and is expected to reach USD ~63 billion by 2035 globally, backed by sustainable agricultural practices.

GLOBAL SPECIALTY FERTILIZERS MARKET (2016-2035)

Source: Frost & Sullivan Analysis

Key Growth Drivers for Specialty Fertilizers

- Nutrient Efficient: CRF and SRF make the nutrient available for longer periods by reducing nitrogen loss via leaching, thus improving crop yield.

- Environment-Friendly: Delays denitrification by controlling the reaction of soil bacteria with nitrates

- Water Scarcity: Water soluble fertilizers can be applied using drip irrigation techniques, optimizing water usage.

- Sustainability: The use of bio-stimulants reduces the amount of mineral fertilizers introduced into the environment, lowering pollution of soil, water, and air.

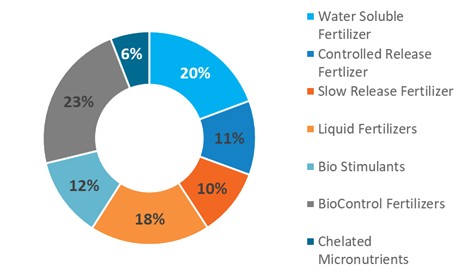

SPECIALTY FERTILIZERS MARKET SHARE, 2023

Source: Frost & Sullivan Analysis

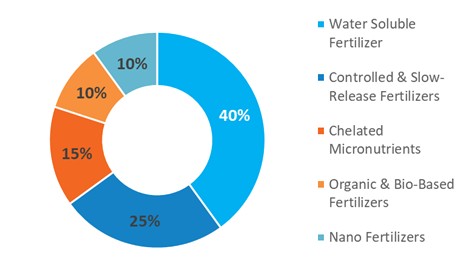

GLOBAL SPECIALTY FERTILIZERS MARKET (2016-2035)

Source: FAI & Frost & Sullivan Analysis

There is a strong need for high-efficiency fertilizers. The implementation of specialty fertilizers is increasing across global market, including the United States, Canada, Brazil, Europe, India, China, and Japan. This is due to the rising awareness about the benefits associated with specialty fertilizers as they are more efficient as compared to standard fertilizers. The use of specialty fertilizers with drip irrigated and other fertigation equipment helps farmers achieve better cost yields effectively.

Driven by increasing adoption of precision and sustainable farming practices, India’s specialty fertilizer market is projected to reach ~5-6 USD billion by 2030, with CAGR of ~18% from 2025-2030 – if Government’s aggressive subsidies and China+1 strategy are effectively deployed. However, Government’s subsidies do not always translate into higher industry value. For example, the Indian controlled-release fertilizer market saw a decline in market value despite increased consumption. The main reason was the Indian government mandating that all domestic urea producers manufacture 100% neem-coated urea and distribute it at subsidized prices to the farmers.

Domestic Players Herald India’s Self-Reliance in Specialty Fertilizers

China’s export halt is set to accelerate India’s self-reliance in specialty fertilizers. Domestic players such as IFFCO, Coromandel, Tata Chemicals, and GSFC are leading the charge, supported by government policies and R&D investments. The supply gap presents immense opportunities to domestic players across all segments of specialty fertilizer demand.

Controlled/Slow-Release Fertilizers: India imported ~200 KTPA of PCU and sulfur-coated urea (SCU).

How are domestic players filling the market gap?

IFFCO’s Nano Urea – A liquid nitrogen alternative reducing urea demand, Deepak Fertilizer’s Nitroplus® – Neem-coated slow-release urea; New start-ups developing lignin-coated urea for delayed nutrient release.

Chelated Micronutrients: India imported ~50 KTPA of Fe/Zn-chelates.

How are domestic players filling the market gap?

Coromandel International – expanded Gromor micronutrient production; GSFC & Aries Argo – ramping up EDTA/DTPA chelates. However, the local production of Fe-EDDHA is still a challenge due to high-tech requirements.

Water-Soluble Fertilizers (WSFs): Disruptions in supplies of MAP & KNO₃ for fertigation.

How are domestic players filling the market gap?

Tata Chemicals is scaling up hydroponic-grade fertilizers; Chambal Fertilizers is increasing soluble NPK blends. New JVs with Israeli firms such as Haifa Group for advanced WSFs are on the horizon.

Organic & Bio-Based Fertilizers: while not halted, reduced the imports of humic acid & seaweed extracts.

How are domestic players filling the market gap?

Aquagro & Biostadt are expanding organic soil conditioners; Camson Bio is producing microbial biofertilizers.

On the technology front, IFFCO and KRIBHCO are leading innovations in nano-fertilizers, while Biostadt and Aquagro are scaling up for Bio-stimulants & precision agriculture solutions.

Conclusion

The Indian specialty fertilizer market is diversifying rapidly, with CRFs, WSFs, and nano-fertilizers driving growth. Government initiatives and China’s export curbs are accelerating domestic production albeit challenges such as Indian specialty fertilizers remain 10-12% costlier than Chinese ones.

The technology gaps in Fe-EDDHA & advanced CRFs require foreign collaboration, for which there are 100% FDI initiative by the Government. Meanwhile, alternatives from Israel’s Haifa Group, Morocco’s OCP Group, Belgium’s Solufeed and Germany’s BASF, are being considered for products including – Polymer-coated urea, Fe-EDDHA/Zn-EDTA, Monoammonium phosphate (MAP) and NBPT-treated urea.

China’s export halt has acted as a catalyst for India’s self-reliance, powered by PM-PRANAM scheme and diversified trade partnerships. However, niche specialties such as high-purity Fe-EDDHA remain difficult to replace entirely.

To connect with Aparajith or Vidhika, please e-mail, Nimisha Iyer at, [email protected]