Global agriculture is entering a period of heightened uncertainty shaped by the convergence of geopolitical instability, climate variability, and rising pressure on productivity. Recent tensions in the Middle East have once again highlighted the vulnerability of agricultural input supply chains that remain heavily dependent on concentrated production hubs, fossil fuel-linked feedstocks, and international trade corridors. At the same time, the growing likelihood of another El Niño cycle threatens to introduce additional volatility into agricultural production systems already operating under resource and economic stress.

Geopolitical Chokepoints and the Fertilizer Supply Shock

The current conflict in the Middle East represents the third major shock to global fertilizer markets in less than six years, following the disruptions caused by the COVID-19 pandemic and the Russia–Ukraine war. A particularly serious concern is the potential for sustained disruptions in fertilizer trade flows through the Strait of Hormuz, which could significantly impact agricultural production cycles and global food security.

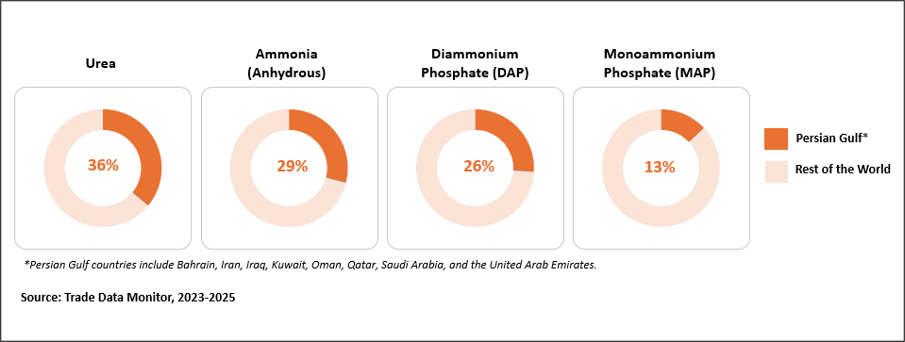

The Strait of Hormuz remains one of the world’s most strategically important trade corridors for both agricultural inputs and energy markets. In 2024, nearly 30% of global fertilizer trade passed through the Strait, alongside approximately 20% of traded liquefied natural gas (LNG) and nearly 27% of internationally traded oil. Any disruption to maritime traffic through this route, therefore, has direct implications not only for fertilizer availability but also for fertilizer production economics globally.

Share of Persian Gulf in Global Fertilizer Exports by Product Type (%), averaged 2023-2025

The role of natural gas is equally important. Natural gas serves both as the primary feedstock and the main energy source for ammonia production, which forms the foundation of nitrogen fertilizer manufacturing globally. Qatar alone accounts for roughly 10% of globally traded natural gas exports, which is the third largest after the US and Australia. South Asian countries, including India, Pakistan, and Bangladesh, rely heavily on LNG imports from the Persian Gulf to sustain fertilizer manufacturing capacity. Higher liquefied natural gas (LNG) prices or reduced availability can increase ammonia production costs, reduce fertilizer output, and ultimately place pressure on fertilizer affordability for farmers. The Persian Gulf region is also a major supplier of sulfur, a critical raw material used in phosphate fertilizer production, accounting for close to 50% of globally traded sulfur supplies according to industry estimates.

Top Importers of Nitrogenous and Phosphate Fertilizers from the Persian Gulf (Metric Tons), 2023

The Food and Agriculture Organization of the United Nations (FAO) has emphasized that the implications of these fertilizer trade disruptions extend far beyond short-term market volatility. The impacts observed today are therefore transmitted forward into future agricultural cycles, potentially affecting food availability well into 2026 and 2027. Importantly, the FAO has also stressed that addressing these risks will require long-term structural transformation across agricultural systems. This includes reducing dependence on concentrated supply routes and fossil fuel-based agricultural inputs through investments in sustainable agriculture, innovative fertilizer solutions, renewable energy integration, and stronger storage and logistics infrastructure.

Climate Cycles Intensifying Pressure on Agricultural Productivity

The World Meteorological Organization (WMO) has projected a rise in Equatorial Pacific sea-surface temperatures between May and July 2026, indicating the emergence of El Niño conditions during this period. The U.S. National Oceanic and Atmospheric Administration (NOAA) estimates an 82% likelihood of El Niño developing between this period and a 96% probability of persistence through the Northern Hemisphere winter (December 2026–February 2027). The timing of this emerging climatic risk is particularly significant, as the El Niño conditions are expected to coincide with ongoing geopolitical disruptions, further affecting global agricultural supply chains.

The implications extend across multiple agricultural commodities like rice, grains, sugar, cotton, palm oil, and soybean. In many regions, climate variability and fertilizer market disruptions can reinforce each other. Weaker monsoon conditions and irregular rainfall patterns associated with El Niño may reduce nutrient uptake capability and increase uncertainty around crop response to fertilizer application. At the same time, higher fertilizer prices can limit farmers’ ability or willingness to apply optimal nutrient levels. Together, these pressures could affect crop productivity and farm economics across several key producing regions.

Expert’s Corner

“Current geopolitical tensions and resulting resource constraints demand a shift away from heavy reliance on inputs toward more efficient and resilient agricultural systems. This transition presents significant opportunities for technologies that improve input efficiency and sustain productivity, including advanced fertilizer and seed treatments, robust soil health solutions, and innovative bio-based interventions.”

Sanika Rajeev Narkar

Research Analyst, Chemicals, Materials, & Nutrition, Frost & Sullivan

Engineering Resilience in Agricultural Systems

As fertilizer supply chains become more vulnerable to trade disruptions, agricultural practices demand a shift from input intensification toward input efficiency and resilience-oriented production models. Frost & Sullivan’s global analysis – Seed and Fertilizer Treatments Market – explores how treatment technologies are emerging as high-impact interventions that improve productivity through targeted input optimization.

The study highlights growth opportunities across emerging controlled-release technologies for precision nutrient applications, as well as sustainable petroleum-free natural and bio-based coatings designed to improve fertilizer performance across nitrogen, phosphate, potash, and blended versions. In addition, the study presents opportunities across seed coating technologies aimed at improving early-stage seed vigor, plant establishment, and nutrient uptake efficiency across all the major crop categories.

Beyond input optimization, long-term agricultural resilience will also depend on improving the health and functionality of the soil itself. Degrading soil quality is increasingly becoming a major concern for agriculture, given soil’s critical role in nutrient retention, water management, microbial activity, and consistent productivity. Against this backdrop, Frost & Sullivan’s global research analysis – Opportunities from the Soil Health Megatrend – is particularly timely.

The study examines the status of soil health while identifying the influence, role, and ongoing efforts of stakeholders across the agri-food value chain. It highlights growth opportunities aimed at improving soil health through biological, organic, inorganic, technology-driven, and agricultural practice-led approaches that support sustainable agricultural outcomes.

The challenges facing the agriculture industry are expected to compound this year, as fertilizer supply disruptions are further intensified by the climate volatility associated with El Niño. There will be an enormous demand for services from companies offering solutions to address these issues, particularly in seed and fertilizer treatments and soil health. This marks an inflection point for the agriculture industry, accelerating the transition toward solutions that enhance input efficiency and strengthen long-term production resilience.

Frequently Asked Questions:

- How do the Middle East tensions impact global agriculture and food production?

Middle East tensions can disrupt fertilizer trade and energy supplies critical for agriculture. Since many countries depend on the region for natural gas and inputs, instability raises costs and limits availability. This can reduce fertilizer use, lower crop yields, and ultimately increase global food prices.

- Why is the Strait of Hormuz important for global fertilizer supply?

The Strait of Hormuz is a vital shipping route for fertilizers, natural gas, and oil. Disruptions here can delay or restrict input supplies worldwide. Since fertilizer production relies heavily on these resources, any blockage can quickly increase costs and reduce availability for farmers.

- How are fertilizer supply disruptions creating demand for alternative crop input solutions?

Fertilizer shortages and high prices push farmers to seek efficient alternatives. Solutions like controlled-release fertilizers, fertilizer coatings improving efficiency, seed treatments, and other bio-based products help improve crop nutrient uptake and maintain yields while reducing input dependence.

- How will El Niño impact demand for crop protection solutions?

El Niño can disrupt rainfall patterns, increasing stress on crops and raising pest and disease risks. These conditions make yields more uncertain, prompting farmers to invest in crop protection solutions to manage risks and safeguard productivity during unstable growing seasons.

- How can farmers make agriculture more resilient to climate change and supply disruptions?

Practices like precision nutrient management with fertilizer treatments, seed treatments for stronger early plant establishment, and soil-health improvement solutions help crops withstand climate stress and resource constraints. Healthier soils and optimized inputs can drive stable, long-term agricultural productivity.

Appendix

For organizations seeking a deeper understanding of the growth opportunities, technology developments, and strategic forces influencing agricultural resilience, productivity, and sustainability, the following Frost & Sullivan analyses provide additional context: