Low fuel prices, high mileage, and reduced maintenance costs consistently emerge as the strongest motivators for current owners, whereas infrastructure gaps and performance concerns slow adoption.

By Shivam Dode, Research Associate – Mobility

Compressed Natural Gas (CNG) adoption in India continues to grow as the country strengthens its push toward cleaner and more affordable mobility. Stable fuel prices in several major cities have helped CNG maintain a cost advantage over petrol and diesel, particularly for urban drivers with high daily mileage. At the same time, government policies and infrastructure expansion are reinforcing CNG’s position as a practical bridge fuel in India’s broader energy transition.

Recent policy initiatives reflect this commitment. The Union Budget 2026 announced the phased blending of Compressed Biogas (CBG) into CNG for transport applications, similar to ethanol blending in petrol. The government also removed excise duty on biogas, a move that could reduce the overall cost of CNG and make it even more attractive for passenger vehicles and commercial fleets. These measures are designed not only to lower emissions but also to reduce the country’s dependence on imported fossil fuels.

Infrastructure expansion is another major focus. India currently has more than 8,600 CNG stations, a sharp increase compared with previous years. The government aims to expand this network to over 18,000 stations by 2030 and significantly increase piped natural gas connections across the country. Corridor-based development along highways and transport routes is also underway to improve fuel availability for both private vehicles and commercial fleets. As infrastructure expands, several automakers are preparing to launch new CNG vehicle models in early 2026, reflecting growing consumer demand for affordable green mobility.

Serious Challenges Lie Ahead

Despite strong policy support and visible progress, India’s plan to build a nationwide CNG ecosystem faces several structural challenges. Establishing a CNG station requires significant investment in compressors, storage systems, and safety equipment, which raises capital costs for operators. These financial barriers are particularly significant in smaller cities where gas pipeline connectivity is still limited.

Land acquisition remains another hurdle. In densely populated urban areas, identifying suitable locations for CNG stations can be difficult, while bureaucratic approval processes often slow down project implementation. These delays make it challenging to scale infrastructure rapidly enough to match growing demand.

Supply-side risks also persist. India still relies heavily on imported natural gas, exposing the market to price fluctuations and geopolitical uncertainties. Delays in domestic gas production projects further constrain supply growth. In addition, regulatory inconsistencies across states and varying safety standards can complicate station approvals and slow network expansion.

In many non-metro areas, the penetration of CNG vehicles remains low, which reduces the financial viability of setting up refueling stations. Competition from electric vehicles is also increasing, while some fleet operators remain hesitant to adopt CNG due to upfront vehicle conversion costs. Execution challenges, including shortages of skilled contractors and limited domestic equipment manufacturing, could further increase project costs and extend timelines.

Understanding Consumer Preferences

To better understand how consumers perceive CNG vehicles, Frost & Sullivan conducted a comprehensive voice-of-customer study titled “Voice of Consumer: Buying Preference of CNG Vehicles in India.” The assessment examined buyer behavior, motivations, and barriers in India’s growing CNG passenger car market.

The research combined quantitative and qualitative insights from consumers across Delhi NCR, Maharashtra, and Gujarat. It included feedback from existing CNG car owners, potential buyers considering a switch to CNG, and individuals who are not currently interested in the technology. The study also incorporated perspectives from automotive OEMs and aftermarket dealers involved in selling and servicing CNG vehicles.

The goal of the study is to provide practical insights for automakers, service providers, financial institutions, and policymakers. As India transitions toward cleaner energy sources, understanding consumer expectations will be critical for expanding the adoption of CNG vehicles and building a stronger supporting ecosystem.

Cost Savings and Mileage Drive Consumer Interest

The study confirms that economic advantages remain the most important reason consumers choose CNG vehicles. Low fuel prices, high mileage, and reduced maintenance costs consistently emerge as the strongest motivators for current owners. These benefits are especially significant for drivers who travel long distances every day, including commercial operators and gig-economy drivers.

Beyond cost considerations, consumers also appreciate the operational characteristics of CNG vehicles. Owners often highlight smooth engine performance, lower noise levels, and the environmental benefits of using a cleaner fuel. Many drivers view CNG as a practical way to reduce both fuel expenses and emissions without making a major shift in driving habits.

Usage patterns further highlight the economic role of CNG vehicles. Approximately one in three current owners uses their cars exclusively for commercial purposes, while many others combine personal use with occasional commercial activities. On average, CNG cars remain in ownership for about four years, reflecting steady but evolving adoption patterns in urban markets.

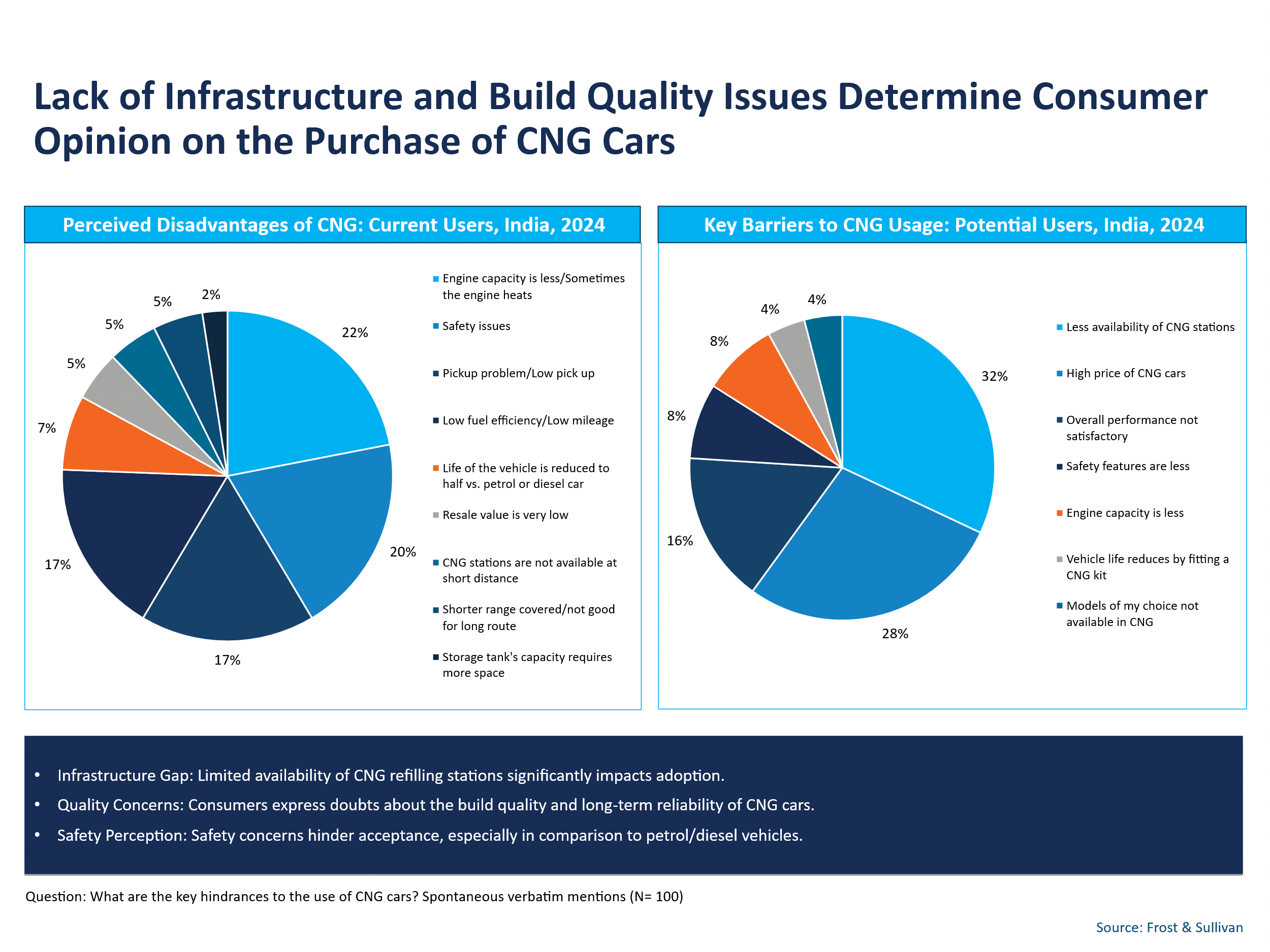

Infrastructure Gaps and Performance Concerns Slow Adoption

While the advantages of CNG are widely recognized, several concerns continue to limit broader adoption. Infrastructure gaps remain one of the most frequently cited barriers. Potential buyers often worry about the availability of refueling stations, particularly outside major cities.

Safety perceptions also influence consumer attitudes. Some drivers express concerns about the long-term reliability and build quality of CNG vehicles, while others remain uncertain about safety compared with petrol or diesel alternatives. These perceptions persist despite improvements in vehicle design and safety standards.

Performance-related concerns also play a key role. Some users believe that CNG vehicles offer weaker engine performance and slower acceleration compared with conventional fuel vehicles. Additionally, the space required for CNG cylinders can reduce available boot storage, which affects the practicality of the vehicle for long-distance travel or family use.

A Dual Market Structure

One of the most distinctive features of India’s CNG passenger car market is the widespread use of retrofit kits. Many consumers prefer to purchase a petrol-powered vehicle and later convert it to CNG in the aftermarket. This approach offers greater cost flexibility and allows drivers to adopt CNG without committing to a factory-fitted model.

As a result, aftermarket retrofitting accounts for a large share of the CNG vehicle base. Up to two-thirds of current users report installing CNG kits after purchasing their vehicles. But in contrast, buying a used CNG car or converting a diesel vehicle to CNG remains relatively uncommon.

At the same time, OEM-fitted CNG vehicles continue to attract buyers who prioritize reliability and warranty coverage. This creates a dual-market structure in which factory-installed systems compete with aftermarket conversions, each appealing to different consumer priorities.

Strengthening the Ecosystem to Accelerate CNG Adoption

Consumer responses in the study underscore several strategies that could help accelerate the adoption of CNG passenger vehicles in India. For instance, the strong association between CNG and cost savings should remain central to marketing and communication efforts. Highlighting long-term fuel savings and lower maintenance costs can strengthen CNG’s appeal among value-conscious consumers.

Product improvements will also play an important role in addressing concerns related to travel range, storage space, and vehicle performance, which could significantly enhance consumer confidence. For example, dual-cylinder designs that reduce the impact on boot space could improve practicality for family use.

Financing access represents another critical area, since retrofitting costs can be a barrier for many potential buyers, particularly in price-sensitive markets. Partnerships between dealers and non-banking financial companies could help create tailored financing options that cover both vehicle purchase and CNG kit installation.

Finally, dealer networks can play a more prominent role in educating consumers about safety, installation quality, and long-term benefits. With proper training and support, dealerships could evolve into full-service hubs that provide retrofitting, servicing, financial assistance, and insurance support.

Strengthening these ecosystem elements will be essential to unlock the full potential of CNG vehicles as an affordable and cleaner mobility solution for India’s cities.

To learn more, please see: Voice of Consumer: Buying Preference of CNG Vehicles in India, or contact [email protected] for information on a private briefing.