New business models leverage vehicle connectivity and real-time data to redefine customer engagement, promote greater fairness and transparency in policies and pricing.

By Parduman Mehra, Industry Analyst – Mobility

Digital technologies are transforming the automotive insurance industry. Previously characterized by static, one-size-fits-all products, the industry is steadily moving toward a more dynamic, data-driven, and customer-centric model. Digital innovation, connected vehicles, and real-time data are redefining how risk is measured, policies are priced, and insurers engage with customers. Automotive insurtech, which marks a convergence of insurance, mobility, and digital technology, is at the center of this transformation.

Moving Beyond a One-Size-Fits-All Approach

This marks a transition from traditional risk pooling that relied on broad proxies such as age, location, declared mileage, and vehicle type to assess risk. Today, that model is being replaced by insurance that responds to real-world behavior. Advances in AI, telematics, IoT, vehicle sensors, and smartphone apps are enabling insurers to assess risk continuously. Connected cars and software-defined vehicles generate rich datasets on speed, braking, acceleration, driving conditions, and vehicle health. This allows insurers to price policies based on actual usage and behavior rather than assumptions. Models such as pay-as-you-drive, pay-how-you-drive, and pay-per-mile are becoming more common, offering fairer pricing and greater transparency.

This shift also reflects changing customer expectations. Insurance customers, especially digital-first younger drivers, want seamless onboarding, app-based policy management, and fast claims settlement. Insurers are responding by modernizing their operations with cloud platforms, embedded insurance APIs, and fully digital customer journeys. At the same time, many drivers remain concerned about data privacy and consent. To build trust, insurers are investing in clearer communication, transparent opt-in mechanisms, and stronger cybersecurity practices.

To learn more, please access: Strategic Shift from Traditional Insurance to Digital Insurance: The Rise of Automotive Insurtech, or contact [email protected] for information on a private briefing.

Technology and Mobility Trends Reshape the Insurtech Landscape

A powerful set of technology trends is reshaping the insurtech landscape. AI, IoT, machine learning, and advanced telematics are helping insurers analyze large volumes of driving data with far greater accuracy. This is improving underwriting and expanding the scope of insurance services, enabling proactive risk management and tailored coverage. These capabilities are changing traditional insurance structures, turning insurance into an always-on service rather than an annual contract and pushing the industry toward faster, more efficient, and more personalized solutions.

Vehicle connectivity is one of the biggest enablers. Modern vehicles increasingly function like software platforms, generating detailed insights into driving behavior, road conditions, and system performance. This data is central to usage-based insurance (UBI) programs, reinforcing the shift toward behavior-linked premiums. Insurers that can effectively access and interpret this data gain a competitive edge, especially as usage-based insurance becomes more mainstream.

Social and mobility trends are also contributing to this evolution. The growth of shared mobility models, including ride-hailing, car-sharing, and subscription models, has increased demand for flexible and short-term insurance. Post-pandemic changes in driving patterns have also boosted interest in low-mileage and on-demand coverage, especially among younger, urban consumers. As ownership shifts toward usership, insurtech providers are embedding insurance into leasing, rental, and mobility platforms, creating smooth, integrated experiences.

Focus Shifts from Static Policies to Real-Time Risk Management

Insurtech is redefining insurance from a reactive service into a proactive, continuous risk management system. Traditional pricing relied on declared information and periodic reviews. In contrast, digital insurance assesses risk continuously based on real-time behavior. Advances in telematics and mobile sensing technologies allow insurers to track factors such as acceleration, harsh braking, cornering, trip duration, location, and driving context. These insights support behavior-based pricing, where safer drivers are rewarded with lower premiums. Many programs also provide real-time feedback, coaching tips, and gamified rewards, encouraging better driving habits. This benefits customers through lower costs and insurers through fewer accidents and claims.

Claims management is another area experiencing significant improvements. Automated first notice of loss (FNOL) enables insurers to receive instant alerts when an accident occurs, along with location and severity data. Vehicle sensors and onboard cameras help reconstruct crashes, helping insurers assess impact forces, damage zones, and the sequence of events. This reduces reliance on manual reporting, speeds up claims initiation, and enhances accuracy. Telematics-based verification also makes it harder to file false claims, cutting investigation time and lowering loss costs.

Advanced analytics now support fraud detection, dynamic risk scoring, and policy customization across the insurance lifecycle. Together, these capabilities are creating a more responsive, automated, transparent, and customer-focused insurance ecosystem.

Investments Add to Market Momentum

The global insurtech market is picking up momentum, driven by rising investment and surging adoption of connected vehicle solutions. Funding for automotive insurtech has grown sharply over the last five years, supporting specialized startups and enabling deeper collaboration across the mobility ecosystem. This influx of capital is accelerating innovation and the rollout of telematics-driven products.

Usage-based pricing is gaining widespread traction. More than 40 million vehicles worldwide already use telematics-enabled insurance features, and UBI adoption is expected to exceed 200 million vehicles by 2030. Safe drivers are seeing notable reductions in their premiums, making these programs attractive to cost-conscious consumers while giving insurers access to more reliable risk data.

AI and predictive analytics are playing an increasingly central role in fraud prevention, underwriting improvement, and dynamic pricing. Machine learning models can significantly reduce fraud and improve loss ratios through more precise risk classification. Meanwhile, innovations such as automated FNOL, blockchain-based data sharing, and digital claims management are shortening claim cycle times, enabling faster settlements and better customer satisfaction.

Partnerships across the mobility ecosystem are becoming more common. Insurers are working with automakers, payment providers, mobility platforms, and smart city providers to offer integrated mobility-as-a-service solutions. Connected security technologies are also improving stolen vehicle recovery rates and supporting predictive theft prevention.

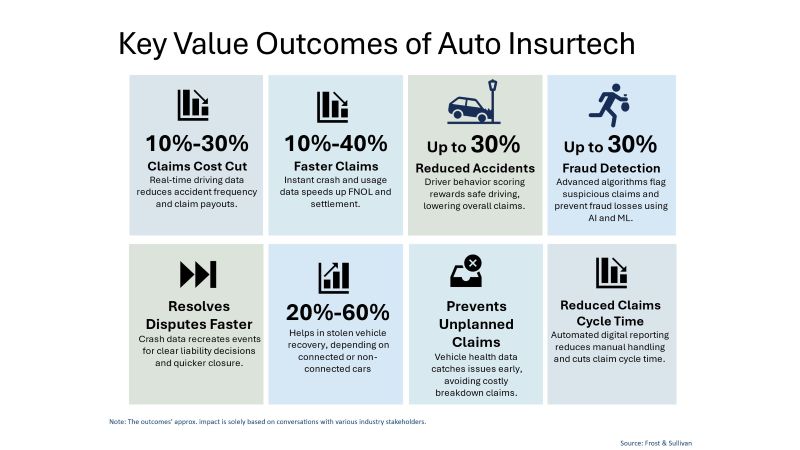

Outcomes Highlight Superior Functionality and Value*

Telematics, AI, connected sensors, and blockchain are delivering measurable benefits for insurers, OEMs, and drivers. Real-time driving data has reduced claims costs by 10–30% and theft losses by up to 40%. Safe drivers can save as much as 25% on premiums.

Claims handling has become significantly faster. Continuous data sharing can cut processing times by up to 40%, with simple claims often settled in under a week. Behavior-based scoring programs are reducing accident frequency by as much as 30% for drivers engaged in safe-driving programs. AI-driven underwriting improvements and capabilities in predicting fraud patterns are supporting loss ratio gains of 3–10%. Accident reconstruction tools are reducing disputes and legal costs by enabling quicker liability assessments.

Blockchain is beginning to secure policy and claims data through tamper-proof records, lowering fraud risk and simplifying approvals. GPS-based stolen vehicle recovery systems are achieving recovery rates of up to 70%, while predictive maintenance tools help prevent costly breakdowns and reduce warranty costs for OEMs. Ecosystem partnerships are also boosting service adoption and customer engagement.

Regional Opportunities Vary

Insurtech adoption varies widely by region, creating the need for tailored approaches. In Europe, telematics and AI are helping insurers tackle persistent fraud and vehicle theft, particularly in Southern and Eastern Europe. Embedded insurance models based on partnerships between automotive insurance players and automakers are leveraging connected car data.

North America is poised for significant growth, driven by electric and connected vehicles. Insurers are using AI for automated claims and real-time fraud detection, supported by deep data-sharing relationships with OEMs that enable more accurate usage-based pricing.

In Latin America, high urban theft rates and gaps in traditional insurance coverage create opportunities for smartphone-based telematics and microinsurance models. These solutions provide affordable protection for underserved customers.

India and Southeast Asia are benefiting from a young driver base and high mobile penetration. Flexible usage-based insurance, combined with claims triage through popular messaging platforms, is enabling insurers to deliver fast, accessible services. Government-led road safety initiatives are further supporting adoption.

China is moving ahead with AI-enabled fraud detection, facial recognition tools, and close integration between insurers, OEMs, and smart city infrastructure. Strong domestic digital ecosystems make embedded insurance especially scalable.

Growth Prospects Emerge

The insurtech ecosystem includes global insurers, telematics providers, OEMs, mobility platforms, and a growing number of startups. Established players such as Allianz, Progressive, State Farm, Generali, Liberty Mutual, and Octo Telematics, among others, are expanding digital capabilities to gain market share. Competition is intensifying around pricing accuracy, user experience, and the ability to scale across regions.

Growth opportunities are emerging across several areas. UBI remains central as customers seek fairer and more transparent options. Collaboration between insurers, OEMs, and digital solution providers will be critical, supported by clear data privacy frameworks. Another major opportunity lies in driver engagement and risk coaching. Real-time feedback and gamified programs help improve driving habits and strengthen retention by turning insurance into an ongoing service rather than an annual transaction.

Regional customization is another critical growth lever. Local partnerships allow global insurers and OEMs to adapt products to different regulatory environments and driving behaviors. Custom-built apps, localized data models, and region-specific claims services accelerate adoption and create a differentiated customer experience.

Advanced claims management and fraud prevention present a high-impact opportunity. AI, connected vehicle data, and automated crash detection can transform claims from a slow, manual process into a fast, data-verified service that reduces fraud, speeds up settlements, and builds consumer confidence. Clear frameworks for secure data sharing between OEMs, insurers, and regulators will be essential to scale these solutions responsibly and sustainably.

(*figures mentioned in the section are based on interviews conducted with stakeholders as part of primary research)