The Indian passenger vehicle HMI market is transitioning toward integrated, immersive, and personalized digital platforms that enhance the user experience and support long-term value.

The passenger vehicle human-machine interface (HMI) market in India is transforming rapidly as vehicle cabins become increasingly digital, connected, and software-driven. Rising smartphone penetration, accompanied by changing customer expectations, is resulting in drivers now seeking seamless and intuitive digital experiences inside their vehicles.

This shift has moved the market away from traditional, button-heavy dashboards toward touchscreen-centric and voice-enabled digital cockpits. These new architectures integrate infotainment, navigation, telematics, and connected services within unified interfaces. The transition reflects a broader shift toward software-defined vehicles (SDVs), with HMI playing a critical role in enhancing user engagement and safety compliance while enabling convenient over-the-air (OTA) feature upgrades.

Overall, the Indian passenger vehicle HMI market is evolving toward immersive and personalized digital cockpit solutions. As OEM competition intensifies across both premium and mass-market segments, HMI capability is emerging as a key differentiator.

To learn more, please see: Passenger Vehicle Human-Machine Interface (HMI) Market, India, 2025, or contact [email protected] for information on a private briefing.

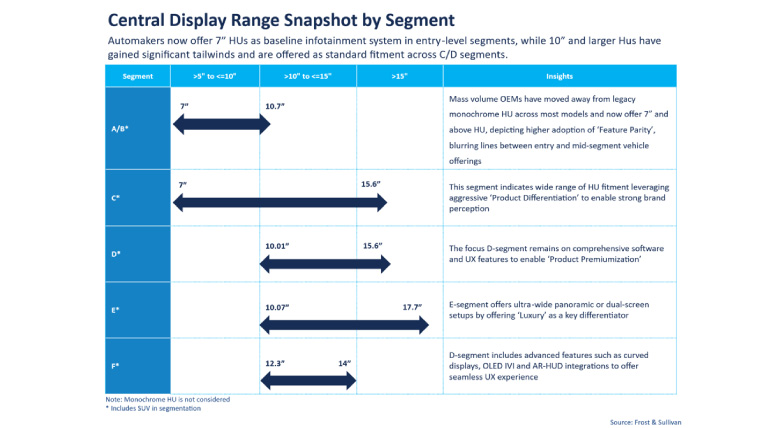

Vehicle Cabin is Transforming into a Personalized Digital Hub

A key driver of HMI adoption in India is the growing demand for connected services, fueled by widespread smartphone usage and increasing digital literacy. In-vehicle infotainment has become a keystone of HMI systems, transforming the vehicle cabin into a personalized digital hub or “third living space.” Longer commute times have further strengthened demand for engaging and connected in-car experiences.

The move toward smart and software-defined infotainment stacks is also reshaping the competitive landscape. Today, automakers and suppliers are increasingly adopting Android-based operating systems, cloud-connected platforms, and OTA update capabilities. These systems support subscription-based services, enabling OEMs to unlock new revenue streams beyond vehicle sales. The expansion of 4G and 5G networks, along with improving cloud infrastructure, is further accelerating adoption by enabling richer content and more accurate navigation, along with real-time vehicle services.

However, the market faces notable challenges. Advanced processors and high-resolution displays significantly increase system costs, which are often passed on to consumers. High data subscription expenses can discourage sustained use of connected features.

Additionally, cybersecurity risks are rising as vehicles become more connected, while India’s Digital Personal Data Protection Act, 2023 introduces uncertainty around data collection, storage, and usage practices. Poor user experience related to slow boot times and outdated hardware acts as a limitation in low- and mid-segment vehicles, which comprise a major user segment for HMI systems.

Electric Vehicles (EVs) are Influencing HMI Design and Functionality

One of the most significant trends in the Indian HMI market is the migration toward software-defined platforms. OEMs are adopting centralized computing architectures and Android-based operating systems to enable scalability, localization, and continuous feature upgrades. In addition to improved interface responsiveness, these platforms facilitate the deployment of new applications and security updates without frequent hardware changes, strengthening long-term product value.

Feature democratization is another defining trend. Technologies like large floating touchscreens, connected navigation, and voice-based assistants that were once exclusive to premium vehicles are now increasingly available in mid-range and entry-level passenger vehicles. This shift is intensifying competition among OEMs and Tier I suppliers and accelerating innovation cycles across the market, even while narrowing the gap between volume and premium segments.

Electrification is further influencing HMI design and functionality. EV launches are accelerating innovation in HMI architecture across the Indian market. EVs typically showcase next-generation digital cockpits that provide real-time system insights, including battery charging analytics and energy visualization. As a result, EV platforms are driving the adoption of fully digital and visually immersive cockpits. OEMs are increasingly leveraging these advanced HMI designs to enhance the user experience in internal combustion engine (ICE) vehicles as well.

A key trend, therefore, is the unification of HMI platforms across EV and ICE portfolios. Several automakers are adopting large displays and centralized hardware architectures originally developed for EVs, then building software variants for different powertrain types. This approach is helping streamline development costs and ensuring brand consistency while creating opportunities for future monetization through software features.

At the same time, regulatory scrutiny around driver distraction, cybersecurity, and data privacy is shaping HMI architecture. It is pushing OEMs toward safer, more intuitive, and compliant interface designs.

Meanwhile, volume OEMs are driving adoption by transitioning base models from monochrome audio systems to Android-based infotainment platforms, enabling a unified HMI experience across vehicle segments. Premium OEMs are extending advanced EV-grade HMI platforms into ICE models to support subscription-based services and scalable digital offerings.

Competitive Landscape is Seeing Deeper OEM–Supplier Collaboration

The Indian passenger vehicle HMI market is characterized by strong participation from global Tier I suppliers working closely with both domestic and international OEMs. Leading suppliers such as Harman, Visteon, Continental, Forvia (Clarion), Panasonic Automotive, Bosch, and Denso provide infotainment systems, digital cockpit solutions, and embedded software platforms. In addition to their global scale, their competitive advantage lies in deep software expertise and well-established OEM relationships.

OEMs including Maruti Suzuki, Hyundai, Tata Motors, Mahindra, Kia, Toyota, Volkswagen Group, BMW, Mercedes-Benz, and Audi, among others, play a pivotal role in defining HMI specifications and technology roadmaps. Rather than hardware alone, OEM–supplier partnerships are increasingly focused on software ecosystems, AI-enabled interfaces, OTA capability, and cybersecurity compliance.

The market is moving toward deeper collaboration, with platform flexibility and software readiness emerging as critical differentiators. Suppliers that can support long-term software updates, regional customization, and scalable architectures are better positioned to succeed as the industry transitions toward SDVs.

Focus on AI-Driven Personalization

Personalization and AI-driven intelligence represent a major focus area for the future. OEMs are investing in intelligent cabin platforms that leverage user data analytics and multimodal interaction, including voice, touch, and gesture controls. AI-based personalization can enable mood-based experiences, adaptive interfaces, and context-aware services, thereby driving uptake.

Immersive infotainment and multisensory UX design are also gaining traction. OEMs and display suppliers are exploring scalable display architectures that support flexible interface layouts and richer visual experiences. Partnerships with content providers and app developers are enabling safer, seamless integration of advanced navigation and infotainment, while multisensory elements such as acoustic tuning and tactile feedback are set to boost comfort and brand differentiation.

Another promising growth area is in-vehicle wellness and comfort-as-a-service. Advanced sensor networks and biometric systems can interact with HMI platforms to deliver adaptive comfort features, including stress monitoring and personalized cabin settings. Rising consumer interest in health-focused mobility presents OEMs and ecosystem partners with opportunities to develop monetizable wellness services aligned with safety and regulatory standards.