Digitalization of the service ecosystem and rising adoption of alternative fuel trucks are poised to further boost aftermarket expansion globally.

Global medium- and heavy-duty commercial vehicle (CV) sales fell by nearly 4.1% in 2025 compared to the previous year. This was largely due to weak freight demand and cautious fleet spending, amidst broader economic uncertainty across major markets. Meanwhile, high operating costs and vehicle prices, aggravated by tighter financing conditions, also discouraged large-scale fleet replacement activity. This slowdown in new truck purchases is expected to persist through the first half of 2026.

Despite weaker truck sales, the CV aftermarket remained resilient in 2025. Global aftermarket revenue increased by 4.9%, with Asia-Pacific and Latin America recording the strongest year-over-year (YoY) growth. This is related to fleet operators across regions attempting to manage costs by extending vehicle ownership cycles and retaining trucks for longer periods. As a result, demand for replacement parts, repair services, and maintenance solutions has continued to rise steadily.

Global vehicles-in-operation (VIO) is projected to grow by 1.6% in 2026 as fleets continue to add vehicles gradually, while delaying large replacement cycles. Simultaneously, updated tariffs and changing trade agreements, particularly in North America and Latin America, are placing pressure on supply chains and parts pricing. This is encouraging fleet operators to seek more affordable alternatives, while creating stronger opportunities for independent aftermarket (IAM) suppliers. From mid-2026 onward, improving freight activity, fleet renewal demand, and increasing adoption of alternative fuel trucks are expected to boost aftermarket expansion globally.

Moving Toward Uptime and Digital Services

The CV aftermarket is rapidly evolving from a traditional repair-focused model into a proactive uptime-driven ecosystem. Fleet operators are increasingly prioritizing vehicle availability and predictive maintenance rather than relying only on reactive repairs. OEMs and service providers are responding by expanding remote diagnostics and data-driven maintenance solutions that help reduce unplanned downtime and improve operational efficiency. Overall, this is promoting a lower total cost of ownership.

Meanwhile, software-defined vehicle (SDV) platforms and over-the-air software updates are also transforming aftermarket operations. They are allowing OEMs to remotely deliver diagnostics, software fixes, feature upgrades, and performance improvements without requiring workshop visits. This shift is gradually moving aftermarket revenues towards digital subscriptions and connected services, as well as OEM-led service platforms.

At the same time, aftermarket supply chains are becoming more regionalized and automated. Besides reducing tariff risks for suppliers, nearshoring strategies are improving parts availability and delivery times by moving production closer to major end markets. In parallel, the growing adoption of robotics, AI, and automated warehousing systems is enabling faster response times for customers. Together, these developments are resulting in a more technology-enabled and service-oriented aftermarket.

To learn more, please see: Growth Opportunities for the 2026 Medium- and Heavy-Duty Commercial Vehicle Aftermarket, or contact [email protected] for information on a private briefing.

Rising Vehicle Age and Utilization Are Increasing Parts Demand

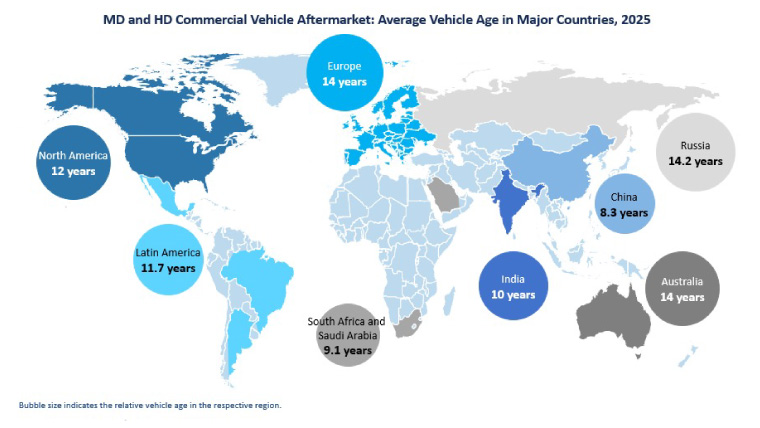

In 2026, global average aftermarket spending per truck is projected to increase by 3.5%, supported by higher fleet utilization, aging vehicles, and rising parts costs. Many operators are delaying new truck purchases and continuing to operate older vehicles for longer periods, particularly in Europe and Latin America. This trend is spurring demand for parts replacement, repairs and maintenance services.

Tariffs on imported vehicles and components are also contributing to higher aftermarket spending. Countries such as the US, Brazil, and Mexico continue to impose import duties ranging from 25% to 50% on certain vehicles and auto parts. These additional costs are intensifying pricing pressure across the aftermarket value chain and prompting demand for more cost-effective, locally sourced components and IAM products.

Regionally, North America and Asia-Pacific are expected to account for a growing share of aftermarket revenue in 2026. Demand growth in other regions will remain comparatively moderate. Opportunities will continue to emerge through fleet expansion and infrastructure investments, along with the need for regulatory-driven upgrades.

Strong Revenue Growth Expected Through 2026

Global replacement parts revenue is expected to increase by 5.2% year over year in 2026, notwithstanding continuing uncertainty in freight transportation demand. Asia-Pacific, North America, and Europe are likely to remain the largest revenue contributors, while Europe is anticipated to record the fastest growth rate at nearly 6.0%. A rebound in China and sustained expansion in India are also anticipated to strengthen aftermarket demand across Asia.

Government policies and incentives will continue influencing market dynamics. China’s expanded scrappage and trade-in incentive programs are set to encourage the retirement of older high-emission trucks and support the purchase of newer vehicles. Meanwhile, accelerating electric truck adoption in China, regulatory-driven fleet transitions in Europe, and gradual EV growth in the US will begin impacting aftermarket demand. Although internal combustion engine (ICE) vehicles will continue dominating the market, demand for EV-related components and services is expected to grow steadily.

Connected vehicle technologies, IoT, and real-time data analytics will motivate OEMs to integrate AI-enabled diagnostics, predictive maintenance, and remote servicing capabilities into their aftermarket strategies. However, trade tensions, especially those involving US tariffs on imported trucks and parts, will continue to create supply chain disruptions. They will result in pricing volatility and margin pressure across the global CV aftermarket value chain.

Looking Beyond Traditional Parts Sales

From 2027-2031, the global medium- and heavy-duty CV aftermarket is projected to grow at a CAGR of approximately 6.1%. Growth will be supported by stable VIO expansion, rising per-vehicle spending, and increasing demand for connected services. Aftermarket participants are expected to focus more heavily on software integration, predictive maintenance, telematics, and recurring service-based revenue models.

Meanwhile, the shift toward alternative fuel vehicles will create new opportunities across the aftermarket ecosystem. Stricter emissions regulations, carbon reduction targets, and rising diesel prices are encouraging fleet operators to adopt electric, CNG, LNG, and hydrogen-powered trucks. The use of electric medium-duty trucks in urban delivery and short-haul operations will boost demand for EV-specific components. At the same time, alternative fuel vehicles will require specialized diagnostics, safety procedures, and technician training. OEMs will therefore need to hike investments in workforce training and specialized servicing capabilities.

The CV service landscape remains highly fragmented among OEMs, dealers, independent workshops, distributors, and fleet operators. Digitalization of the service ecosystem is, therefore, becoming another major growth area. Connected digital platforms will help integrate diagnostics, service scheduling, parts ordering, and maintenance history into a single ecosystem. OEMs will need to fast-track the development of centralized digital service platforms, while partnerships with technology firms will be needed to accelerate SDV adoption and predictive maintenance solutions.

Regulations such as EPA Phase 3, Euro VI/VII, China VI, and Bharat Stage VI are highlighting the need for emissions compliance throughout a vehicle’s operating life. Accordingly, lifecycle emissions management will emerge as a long-term revenue opportunity for OEMs. Emission health contracts, software recalibration services, sensor replacement programs, and connected diagnostics will create recurring revenue streams. In parallel, truck service centers will likely expand capabilities in diesel particulate filter (DPF) cleaning, sensor remanufacturing, and emission system validation to address growing service demand.