Advances in vehicle connectivity, AI-driven perception, and smart infrastructure, together with rising consumer demand for safety and convenience is set to boost uptake of auto park assist (APA) and automated valet parking (AVP) systems.

By Parduman Mehra, Industry Analyst – Mobility

Passenger vehicle automated parking systems are rapidly moving from being niche convenience features to becoming mainstream offerings. From simple ultrasonic-based assistance, these systems are becoming increasingly capable of navigating complex parking environments with minimal or no driver intervention. This reflects broader shifts in the automotive industry toward software-defined vehicles (SDVs), AI-driven decision-making, and connected mobility ecosystems.

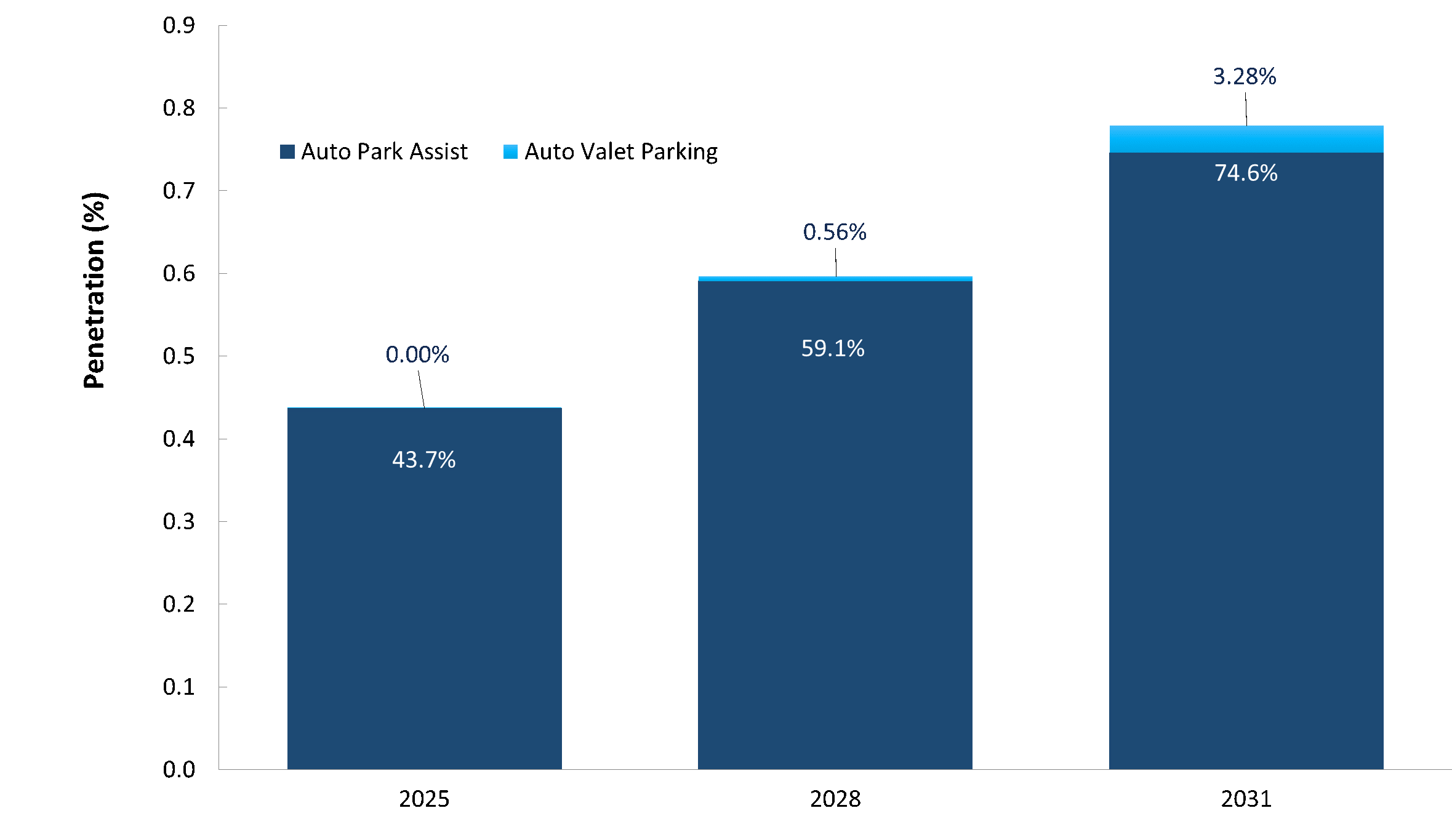

Between 2025 and 2031, the global automated parking systems market is set to expand significantly, driven by growing consumer demand for stress-free parking and steady improvements in sensing and computing technologies. As costs decline and advanced driver assistance systems (ADAS) hardware become standardized, automated parking will move beyond premium vehicles and steadily penetrate mass market segments. Here, while Auto Park Assist (APA) systems are already widely available, more advanced Automated Valet Parking (AVP) solutions are transitioning from controlled pilots to early commercialization.

Market growth is being supported by smart infrastructure investments and regulatory momentum in key regions. Governments and city planners are increasingly viewing automated parking as part of a broader solution to urban mobility challenges, including limited parking space. Together, these factors are highlighting the role of automated parking as a key capability in next generation passenger vehicles.

For more information, please see: Passenger Vehicle Automated Parking Systems Market, Global, 2025–2031, or contact [email protected] for information on a private briefing.

Sensor Fusion is Enabling Smoother, Safer Parking Performance

Early automated parking technology systems relied heavily on ultrasonic sensors and predefined maneuvers. They offered limited reliability in complex or crowded spaces. In contrast, today’s solutions integrate cameras, radar, and increasingly LiDAR, supported by high-performance computing platforms. These technologies enable precise vehicle localization, real-time perception, and memory-based parking. This sensor fusion approach allows vehicles to interpret their surroundings more accurately, enabling smoother, safer parking performance.

A crucial shift has been the transition from hardware-led differentiation to software-driven value creation. Perception algorithms, AI-based path planning, and low-speed decision-making logic are becoming primary sources of competitive advantage. OEMs and Tier 1 suppliers are leveraging over-the-air (OTA) updates, allowing for continuous improvements to parking performance even after vehicle purchase.

Amidst the shift towards SDVs and software-centric models, traditional Tier 1 suppliers such as Bosch, Continental, ZF, and Valeo are collaborating with semiconductor and AI specialists, including NVIDIA, Qualcomm, and Mobileye. At the OEM level, global automakers and EV-focused brands are integrating automated parking as a differentiating feature, particularly in premium and electric vehicle (EV) segments. This ecosystem of suppliers, technology enablers, and OEMs is accelerating innovation while driving down system costs.

European Market Leads with Clear Regulation and Pilot Deployments

The market is estimated to grow from around 26 million units in 2024 to 56 million units by 2031. Frost & Sullivan projects APA penetration to reach nearly 74.6% by 2031, reflecting its transition into a mainstream feature. In contrast, Level 4 AVP systems will remain limited in volume but are expected to achieve early commercial deployment in premium and EV models.

In regional terms, the market in North America continues to benefit from strong consumer acceptance of ADAS features, flexible regulatory conditions, and installation in premium vehicle models. Meanwhile, close collaboration between OEMs, technology providers, and parking infrastructure operators will enable cloud-based updates and feature enhancements, motivating uptake. Accordingly, semi-automated parking penetration in North America is expected to be just over 70% by 2031.

Europe has been a frontrunner with its progressive regulations and pilot deployments. Supportive UNECE frameworks and national legislation like Germany’s StVG, reinforced by pilots from Mercedes-Benz and BMW, have enabled early Level 4 AVP trials. Adoption is expected to rise rapidly, driven by premium vehicle segments and urban smart mobility initiatives. Accordingly, automated parking penetration is poised to increase from 45% in 2025 to more than 75% by 2031, led by the premium segments.

China, Japan, and South Korea are at the vanguard of market growth in the Asia-Pacific region. Strong government support for smart mobility programs, OEM-tech ecosystem integration, localized sensor and AI supply chains, and strong urban demand are among the main factors that will push automated parking installation to surpass 70% of new vehicles by 2031.

Smart Infrastructure and Cost Reduction to Accelerate Market Development

The integration of automated parking systems with smart infrastructure is becoming a critical growth enabler, especially for AVP solutions. Infrastructure-aided parking relies on vehicle-to-infrastructure communication and smart garage integration to coordinate safe and efficient vehicle movements. Pilot projects in Europe and Asia-Pacific that integrate IoT sensors and cloud-based management systems are underscoring the ability of connected parking facilities to improve the reliability of automated parking solutions.

Cost reduction is another major factor accelerating market expansion. As cameras, radar, and compute platforms are increasingly shared across multiple ADAS functions, the incremental cost of adding automated parking features continues to fall. Feature-level costs for APA are expected to drop below $150, while AVP systems are forecast to fall below $350. These declines will underpin the transition to mass market scalability.

The rise of EVs will further strengthen the business case for automated parking. Autonomous positioning within parking facilities is expected to optimize the use of charging infrastructure by reducing the time taken to correctly occupy a charging space and thereby improving charger turnover. Such capabilities will be a major asset for parking lot operators and infrastructure partners in high-demand areas.

Unlocking Growth in the Next Phase

Looking ahead, AI-driven perception and decision-making will be central to unlocking the next phase of automated parking adoption. Advanced deep learning models can address edge cases that challenge today’s systems, such as irregular parking layouts, poor lighting, or ambiguous obstacles. Enhancing reliability in these scenarios will be essential for building consumer trust and securing regulatory approval for higher levels of automation.

Automated parking also represents a strong opportunity for digital monetization. Consumers are increasingly recognizing the tangible value of time savings, reduced stress, and lower risk of minor collisions. As a result, APA and AVP are well suited to subscription-based business models. OTA activation will allow OEMs to offer parking features post-sale, creating recurring revenue streams and extending customer lifetime value.

Frost & Sullivan sees China as playing a decisive role in shaping the future landscape of the global automated parking market. Severe parking constraints in its megacities, combined with aggressive smart city and connected vehicle initiatives, will position AVP as a core component of the country’s mobility strategy.

Ultimately, OEMs, Tier 1 suppliers, and technology providers that localize development, align with national connectivity standards, and tailor monetization models to regional preferences will be best positioned to capture long-term growth in this rapidly evolving market.